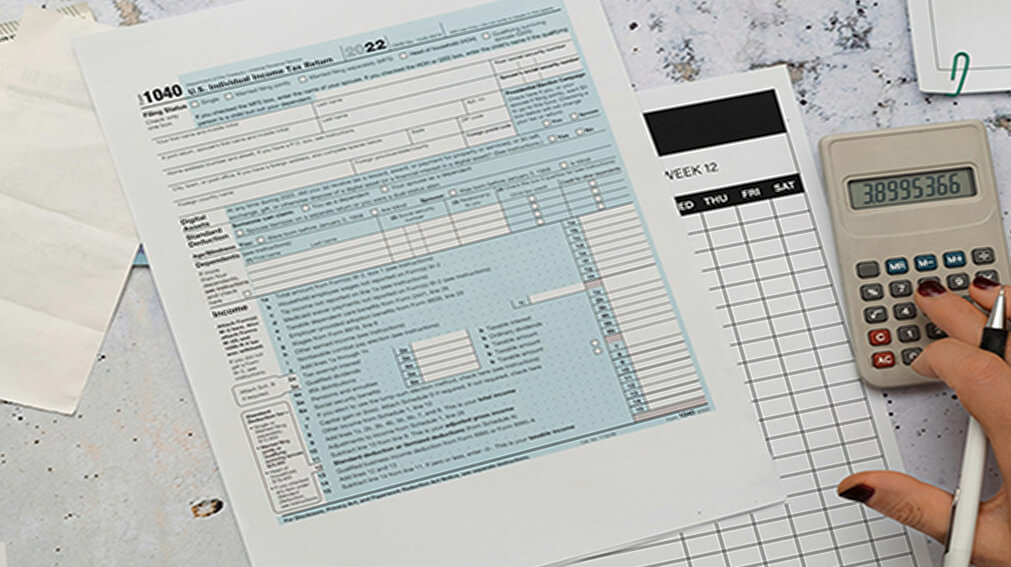

RLTYco has partnered with Block Advisors & Nimbl to provide real estate agents the support they need come tax season. Whether filing as an individual or as a business, work with RLTYco to streamline your taxes and get every credit and deduction you deserve.

For real estate professionals operating as independent contractors, single member LLCs, S Corps and more. Save money by working with a Block Advisors’ small business certified tax professional.

Meet with a tax professional from Block Advisors in person or online

Ready to get started?

Download your RLTYco coupon here

File online and on your own time through the Block Advisors website

Meet with a tax professional from Block Advisors in person or online

Ready to get started?

Download your RLTYco coupon here

Meet with a tax professional from Block Advisors in person or online

Ready to get started?

Download your RLTYco coupon here

File online and on your own time through the Block Advisors website

Similar to an LLC, a corporation is a business entity that helps protect personal assets but has more flexibility on ownership

Provide for your loved ones by planning for the future while avoiding probate court

Provide for your loved ones by planning for the future

Limited Liability Company (LLC)

A simple way to structure your business. An LLC helps protect your personal assets and provides more tax flexibility.

Corporation

Doing Business As (DBA)

Stay in compliance with a registered agent for your LLC or Corporation

Provide for your loved ones by planning for the future while avoiding probate court

Similar to an LLC, a corporation is a business entity that helps protect personal assets but has more flexibility on ownership

Provide for your loved ones by planning for the future while avoiding probate court

Provide for your loved ones by planning for the future

Meet with a tax professional from Block Advisors in person or online

Ready to get started?

Download your RLTYco coupon here

File online and on your own time through the Block Advisors website

Tax Prep + Year-Round Email Support

Tier 1 + Annual Tax Planning

Tier 2 + Quarterly Planning & Estimates

Meet with a tax professional from Block Advisors in person or online

Ready to get started?

Download your RLTYco coupon here

File online and on your own time through the Block Advisors website

File online and on your own time through the Block Advisors website

File online and on your own time through the Block Advisors website

Meet with a tax professional from Block Advisors in person or online

Ready to get started?

Download your RLTYco coupon here

Limited Liability Company (LLC)

A simple way to structure your business. An LLC helps protect your personal assets and provides more tax flexibility.

Corporation

Doing Business As (DBA)

Stay in compliance with a registered agent for your LLC or Corporation

Provide for your loved ones by planning for the future while avoiding probate court

Similar to an LLC, a corporation is a business entity that helps protect personal assets but has more flexibility on ownership

Provide for your loved ones by planning for the future while avoiding probate court

Provide for your loved ones by planning for the future

For agents who want to get organized and stay organized

Agents looking to do their own bookkeeping

For Agents looking for professional bookkeeping help

Starting at

For agents with complex bookkeeping needs

Schedule a free consultation with Block Advisors and receive your first month of Full Service or Premiums packages, plus 10% every month after that

Services offered through Block Advisors by H&R Block. By visiting Block Advisors, you are leaving RLTYco.com, and your information will be subject to their privacy policy

H&R Block’s small business tax professional certification is awarded by Block Advisors, a part of H&R Block, based upon successful completion of proprietary training. Block Advisors’ small business services are available at participating Block Advisors and H&R Block offices nationwide.

*Discount valid at participating Block Advisors or H&R Block U.S. offices for an original 2024 income tax return for new clients only, and may not be combined with any other offer or promotion. Coupon must be presented prior to the completion of initial tax office interview. A new client is an individual or business who did not use Block Advisors or H&R Block to prepare their income tax return within a year from the date of the 2024 income tax return preparation. Void if transferred and where prohibited. No cash value. OBTP#B13696-BR ©2025 HRB Tax Group, Inc

**Valid for H&R Block Online for an original 2024 personal federal income tax return for new clients only. Discount may not be combined with any other offer or promotion. H&R Block Online must be accessed from the included link, and discount will be applied automatically at checkout. A new client is an individual or business who did not use Block Advisors or H&R Block to prepare their income tax return within a year from the date of the 2024 income tax return preparation. Void if transferred and where prohibited. Exclusions may apply. No cash value. OBTP#B13696-BR ©2025 HRB Tax Group, Inc.

(1) Up to 30% savings reflects average savings based on national average fees for Federal Form 1040 plus Schedule C and one state filing in latest available 2020 survey conducted by the National Society of Accountants. All tax situations are different. Pricing will vary based on individual circumstances.

(2) Up to 50% savings reflects average savings based on national average fees for Federal Form 1065, 1120, and 1120S in latest available 2020 survey conducted by the National Society of Accountants. All tax situations are different. Pricing will vary based on individual circumstances.

(3) Your Block Advisor or H&R Block accountant may not be a licensed accountant

(4) First month free offer valid for virtual Premium or Full-Service bookkeeping services, up to $175, excluding one-time set up fees. Following the first month, you will be charged then-current monthly rates, minus a 10% discount, until you cancel the discounted service(s) or terminate your client service agreement. Cancel or terminate before the end of your first month to avoid recurring charges. We reserve the right to change the standard monthly rates at any time. Offer is valid for new clients only.

A new client is an individual or business who has not used Block Advisors for bookkeeping services. Discount may not be combined with any other offer or promotion. Void if transferred and where prohibited. No cash value. © 2025 HRB Tax Group Inc.

Block Advisors’ Bookkeeping Full-Service plans include your own dedicated account manager, income and expense management, easy receipt capture, review of books year-to-date, standard chart of accounts, and custom financial statements.

Premium plans also include inventory, mileage, and expense management tools, project tracking, quotes, estimates, custom chart of accounts, accrual-based accounting, sales and use tax filing, and multiple currency options.

“Lifetime” or “for life” refers to the life of your client service agreement with Block Advisors for bookkeeping services. If your bookkeeping services are cancelled for any reason, including termination of your client service agreement, you will no longer be eligible for the 10% discount for bookkeeping services. That means you will not be able to reengage the offer if you choose to restore bookkeeping services at a later date. Please note that although you will receive a 10% discount off the then-current monthly rates for the bookkeeping services, Block Advisors reserves the right to change monthly rates at any time.